Cassandra Beitel

Cassandra has accumulated a myriad of marketing experience over the past (nearly) 10 years, giving her a well-rounded perspective of data analysis, client-side and agency-life. When she's not planning holistic media strategies, you'll find her at the Crossfit box, hanging out with her dog (Jasper), or spending time outside.

COVID Continued: Media and Consumer Behaviour Shifts Part 3

Here we are, entering December and COVID is still ever present. I never thought I would be writing a part 3 to our ongoing COVID series. We first shared an update on The Shifting Media Landscape Amidst the COVID-19 Pandemic in April followed by How are Consumers Changing with COVID-19 in May. Our lives have continued to shift and change throughout the pandemic and we’ve adapted: in Alberta we locked down in March, moved into looser restrictions over the summer (and we all enjoyed a bit more sunshine) and now that the darker cold months are upon us, we’re shifting back into tighter restrictions. Numerator Intelligence surveyed Canadians starting in May 2020 around their sentiment of COVID-19. They found that as the summer passed and as we’ve rolled into winter, Canadian consumers are very concerned about COVID-19, and we anticipate this trend to continue as we get deeper into the winter/holiday season.

The same study found that 46% of Canadians believe that there is an extreme likelihood that there will be a widespread increase of COVID cases over the next two months, with 29% having the primary concern that someone in their household will become infected, which will result in tighter restrictions and a potential surge of bulk/stock-piling items again (23% say they will stock-up on essential items).

In April 2020 we saw a massive dip in consumer spending, with the uncertainty of COVID hitting the world in full force. But despite rising case counts across Canada, consumers continued shopping. Overall spending was up almost 3% in late October and most categories have stabilized. Online spending continued to capture a larger share of spending, with 51% of transactions occurring remotely versus about 46% in mid-summer. 28% of Canadians are very or extremely concerned about their personal finances, whereas 72% are concerned or not very/not at all concerned about their personal finances. Consumers are still planning on spending for the holidays: 15% plan on giving more this year to charitable donations, while 13% plan on spending more for gifts (Source: Angus Reid, Rogers Media, November 11, 2020).

Just as much as our personal habits have shifted, the media landscape continues to change. COVID has brought so much transformation for media and marketing (we’ve talked about these changes here and here, and we are here to talk again about how it’s continuing to evolve. The total advertising spend within Canada has decreased by 8.7% in 2020. With global ad spend projected to decline by 4.5% in 2020 versus pre-pandemic estimates of a 7% growth. However, there is an anticipated rebound for digital ad spend in 2021 of nearly 16.4%, doubling what the traditional media spend is anticipated at – 7.9% growth (Media in Canada, October 29, 2020). With ad spend being lower than anticipated this year, the spend works a little bit harder on channels that we have seen transform during the pandemic.

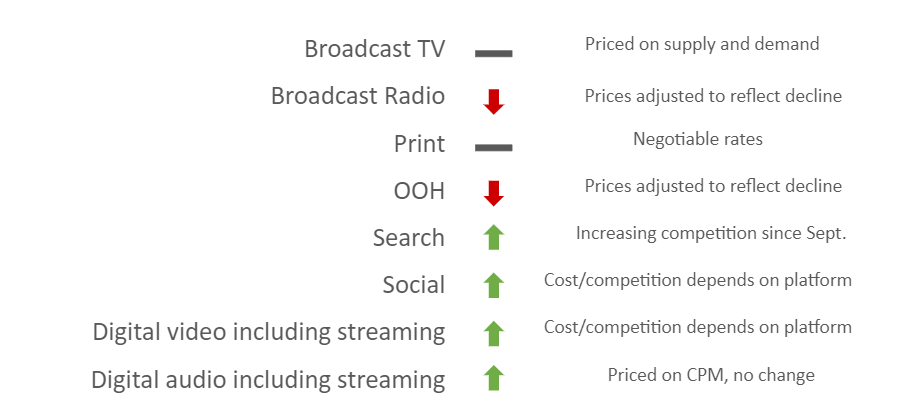

Broadcast and Online TV:

Initially, broadcast television saw an increase in viewing due to an increase in news consumption, to stay informed, increasing across all buying demos. However, once live sports were officially paused, even the increase in news viewership couldn’t offset the decrease in live viewing for TV. Now that we’re into the 10th month of COVID, things have started to normalize; the industry has figured out how to continue to produce new prime-time shows, certain sports are coming back, and the winter weather is sending people inside. A recent study by Vividata shows that 38% of Canadian adults are watching more live TV than they were pre-pandemic, with adults 50% at 43%.

Online TV, which includes subscription services, connected TV and online streaming, continues to increase. At the onset of COVID we saw these channels spike, and they continue to do so, with 52% of Adults under the age of 35 reporting using subscription videos more now than pre-pandemic. With more viewers watching digital videos, inventory is becoming more readily available and spend has increased by 3.6%, even during the pandemic, making up 25.8% of all digital ad spending within Canada.

With broadcast and online TV viewership on the rise, it is an opportunity for marketers to get back into the medium, reaching a wide array of audiences, online and offline. These two platforms intertwine with each other, with broadcast TV carrying a cache of importance, reputability and big spends, while online TV/video reaches a younger audience and allows for tracking and better reporting capabilities.

Broadcast Radio and Online Audio:

Broadcast Radio, which is traditionally consumed while people are in their cars, took a hard hit when the ‘stay in place’ protocols were implemented. In-home listening did see an increase, but not enough to stave off the overall decrease. However, as the restrictions loosened up, broadcast radio slowly started to rebound, with Calgary and Edmonton markets climbing back up (still down YoY though). Where the broadcast radio fell, online audio streaming grew from 2018 (70% of Canadians listened to online audio monthly in 2020 vs. 57% in 2018). Adults under the age of 35 had the highest uptick in streaming services, with 60% reporting greater use of the service during the pandemic; 15% say they are listening to more podcasts, 37% are streaming more music and 35% are listening to more audio books (Numeris, Infinite Dial Canada, https://vividata.ca/company/press-release/ & GloablWebIndex).

Broadcast radio continues to be an excellent way to raise mass awareness to local markets, with most stations having a digital version/online streaming of their service (you can usually get placement on both!). Online audio, which include podcasts and music, has endless capabilities, from standard spots to integrated content within podcasts – again this is an awareness channel, however, some media partners (i.e. Western Media Group) are offering attribution modeling (WMG is LIID) to help better showcase the importance of audio in consumers shopping habits.

Out Of Home:

Similar to broadcast radio, out of home is consumed when consumers are outside of their homes. As vehicular travel plummeted and people stopped going to venues where traditional out of home and indoor ad exposure happens, the consumption of out of home has decreased. As the restrictions loosened people started driving again, which has helped bring back the out of home audiences (average KM travelled daily across Canada has returned to 83% of pre-COVID traffic and is up 28% since April 2020), however, they are still not were they were pre-pandemic. Unfortunately, many of the indoor venues are still continuing to struggle. Due to major events like sports or concerns still being cancelled/not open to the public and restaurants at limited capacity, this is decreasing impressions.

With that though, there is a great opportunity for marketers to secure out of home inventory for 2021 and beyond. Many of the media partners have adjusted pricing to ensure more appropriate CPM’s based on smaller audience numbers and are willing to negotiate on cancellation/shifting policies. Out of home offers a high impact visual for brand campaigns, as well as targetable ads to specific locations (i.e. TSA’s within communities). Additionally, restobars (within age ‘gated’ restaurants/bars/pubs/clubs etc.) are the only way to advertise cannabis in the out of home space (currently). So, to not be too opportunistic, but now is the time to lock in future planning!

Print:

Print was struggling prior to the pandemic, and unfortunately things have not improved. There have been reports that over the past few months of the pandemic there has been lower revenue, more lay-offs, mergers, and publications closing their doors. We do see trends that print consumption/readership is higher on the weekends versus the weekdays; the assumption here is that people have more time to read a physical paper. Many printed publications have a digital edition of their publication, which helps stave off some of the decline. While the outlook for print may seem bleak, over 82% of Canadian adults have read/accessed magazine or news brands in the past week via print or online: 54% of readers consume newspapers on mobile to some degree (up from last year). Community newspaper’s reach remains consistent year over year (42% of all Canadians), showing that consumers still want highly local news that is directly relevant to their lives.

We had previously talked about a decrease in flyers as many retailers shifted their approach to the printed material. Many major retailers such as Canadian Tire paused distribution for a couple of months, while others, such as No Frills and Real Canadian Superstore, discontinued their flyers on a more permanent basis. Retailers have had to shift their focus from printed offers to other more digital channels as consumers are still looking for the best deals, especially as COVID affects household incomes.

Digital Media Habits:

Digital media has been trending upwards for years, as we shift more and more online and COVID-19 expedited that process. Many people are spending more time online, specifically with 70% of Canadians spending more time on their mobile device over the summer than previously. The biggest influx in time spent (outside of online streaming) has been social platforms – people want to stay connected. 43% of Canadians are spending more time on social media (27% increase with A65+), with 42% spending more time messaging; there is a deep human desire to continue the social connections at some level.

With so many people spending more time on messaging apps, they are relying on social media channels to connect with businesses too, and expect responses in a timely manner. 51% of Gen Z and 50% of Millennials have contacted a business via a messaging service, with 19% of Gen Z and 24% of Millennials purchasing through the messaging service (Facebook IQ, Sept 2020). This is a great opportunity for businesses to expand their customer service to younger audiences, keeping in mind that in the digital, everything at our fingertips always, promptness is key!

With consumers spending more time on social media (and online in general), there is more inventory available, which is a double-edged sword – there are more opportunities to reach customers, however, there are now more ads, and the creative/messaging must resonate with your audience to engage and cause an action. Sources for these stats here and here.

Summary:

While the initial onset of the pandemic looked bleak for advertising, things are coming back. Offline media is starting to trend positively again, and digital is still on-top! It’s important for advertisers to remain in-market, even at a low level, to keep awareness of their brand at top of mind; coming out of market completely means eventually when they come back into market, the lifting will be heavier and they will need to spend more to get back to where they were. There is a lot of great opportunity to leverage different channels to speak to the consumer more holistically, be top of mind, and drive eventual conversions (i.e. sales): advertising isn’t going anywhere, just like COVID (though we hope this part changes soon for all our sakes’…).